How to Create a Business Risk Management Plan for Small Companies

What Separates Thriving Small Businesses from the Ones That Close — and Can a Single Document Make the Difference?

A small business risk management plan is a structured document that identifies, evaluates, and prioritizes potential threats to a company’s financial stability, operations, and reputation; it assigns mitigation strategies to each threat based on likelihood and impact. This plan functions as a proactive defense mechanism, converting uncertainty into measurable, manageable variables for resource-constrained enterprises.

Have you ever lain awake at 2 a.m. wondering what would happen to your business if your biggest client disappeared overnight — or if a cyberattack locked every file on your server? You are not alone, and the anxiety is not irrational. The U.S. Bureau of Labor Statistics reports that roughly 20% of small businesses fail within their first year, and nearly 50% do not survive past the 5-year mark. Many of those closures trace back not to a lack of ambition or talent, but to an absence of preparation for the unexpected. Hope, as seasoned financial professionals will remind you, is not a strategy. A documented small business risk management plan transforms vague dread into a concrete action playbook — one you can build on a single Tuesday afternoon. By the time you finish reading, you will know exactly how to identify the threats specific to your company, score them against a practical matrix, choose the right mitigation tactic for each, and compile everything into a living document that could literally save your livelihood.

- Conduct a vulnerability audit with your team — identify 15 to 40 risks across 5 categories: financial, operational, compliance, strategic, and cyber.

- Score each risk using a Likelihood × Impact Matrix (1–5 scale). Risks scoring 15–25 require immediate budget allocation.

- Apply the 4 T’s framework — Tolerate, Treat, Transfer, or Terminate — to every prioritized risk.

- Compile findings into a 8–15 page document: Executive Summary, Risk Register, Action Plans, Roles, and Review Schedule.

- Set quarterly risk review meetings (60–90 minutes). Businesses reviewing quarterly experience 40% fewer uninsured losses.

- Diversify revenue so no single client exceeds 40% of total income.

- Deploy multi-factor authentication (MFA) across all accounts — costs as low as $3/user/month.

- Present your documented plan during loan applications and insurance renewals for better terms.

What Exactly Is a Business Risk Management Plan — and Why Do SMBs Need One?

Let us start with plain language. A business risk management plan is a written record of everything that could go wrong in your company, paired with a clear set of instructions for what you will do about it. Think of it as a fire escape map posted on the wall — except it covers financial fires, legal fires, digital fires, and reputational fires, too.

Large corporations practice what is known as Enterprise Risk Management (ERM), a sprawling discipline overseen by dedicated Chief Risk Officers, internal audit teams, and multimillion-dollar compliance departments. Small and medium-sized businesses (SMBs) do not operate in that world. Your version of a risk management process for small companies needs to be agile, affordable, and focused. It does not require a committee of 40 people or a 200-page report. It requires honesty about your vulnerabilities and a few hours of concentrated thought.

| Comparison Dimension | Enterprise Risk Management (Fortune 500) | Small Business Risk Management (SMBs) |

|---|---|---|

| Team Size | Dedicated CRO, internal audit teams, compliance departments (10–100+ staff) | Owner + 1–3 key staff, plus external accountant or advisor |

| Annual Budget | $500,000 – $10,000,000+ | $0 – $5,000 (mostly staff time) |

| Documentation | 200+ page reports, board-level risk committees, regulatory filings | 8–15 page document with risk register, action plans, and appendices |

| Software Tools | SAP GRC, MetricStream, Archer ($50,000–$500,000/year) | Google Sheets, Notion, QuickBooks ($0–$150/month) |

| Review Cycle | Continuous monitoring with real-time dashboards | Quarterly reviews (60–90 min meetings) + annual comprehensive audit |

| Typical Risk Count | 200–1,000+ identified risks across global operations | 15–40 risks across 5 core categories |

| Framework Used | COSO ERM, ISO 31000, Basel III (financial institutions) | Simplified 5×5 Likelihood-Impact Matrix + 4 T’s framework |

| Time to Build Initial Plan | 6–18 months | 1 afternoon (first draft) to 2 weeks (complete document) |

| Primary Benefit | Regulatory compliance, shareholder assurance, global coordination | Better loan terms, lower insurance premiums, uninterrupted cash flow, confident decision-making |

| Source: Comparison framework adapted from COSO — Enterprise Risk Management: Integrating with Strategy and Performance, Committee of Sponsoring Organizations of the Treadway Commission, 2017 | ||

So what is the return on investment (ROI) for all this effort? Consider the tangible benefits. Banks routinely offer better loan terms to businesses that demonstrate structured financial risk mitigation. Insurance providers may lower premiums when you can prove documented risk controls. Perhaps most significantly, a small business risk analysis keeps your cash flow uninterrupted during crises — because you already know the contingency steps. According to a 2020 survey by the Federation of Small Businesses (FSB) in the United Kingdom, businesses with formal continuity plans were 2.5 times more likely to recover from disruptive events than those without one. That number alone should end any debate about whether the exercise is worth your time.

What Are the 5 Core Types of Small Business Risks to Watch in 2026?

Before you can build a plan, you need to understand what you are planning against. The abstract idea of “risk” becomes far less intimidating once you break it into categories. Here are the 5 domains every small business owner should scrutinize.

| Risk Category | Common Examples | Typical Impact Area | Primary Mitigation Approach | Severity for SMBs (1–5) |

|---|---|---|---|---|

| Financial Risks | Cash flow shortfalls, interest rate hikes, inflation, credit defaults | Revenue, liquidity, profitability | Treat (cash reserves, diversified revenue) + Transfer (credit insurance) | 5 |

| Operational Risks | Supply chain failure, equipment breakdowns, key personnel loss | Production, service delivery, capacity | Treat (cross-training, backup suppliers) + Transfer (business interruption insurance) | 4 |

| Compliance & Legal Risks | Labor law changes, tax regulation shifts (US/UK/AUS), lawsuits | Legal liability, fines, operational disruption | Treat (compliance software, legal counsel) + Transfer (professional indemnity insurance) | 4 |

| Strategic Risks | Competitor disruption, shifting consumer demand, brand reputation damage | Market share, growth trajectory, brand equity | Treat (market research, diversification) + Tolerate (accept residual market risk) | 3 |

| Cyber & IT Risks | Ransomware, data breaches, IT infrastructure failure, phishing | Data integrity, customer trust, regulatory fines | Treat (MFA, firewalls, backups) + Transfer (cyber liability insurance) | 5 |

| Source: U.S. Small Business Administration (SBA) — Business Risk Management Resources, 2024 | ||||

Where Do Financial Risks Hide in Your Day-to-Day Operations?

Cash flow bottlenecks sit at the top of the threat list for most SMBs. A single late-paying client can cascade into missed payroll, supplier penalties, and overdraft fees. In 2024, US inflation hovered around 3.4% year-over-year, and while the Federal Reserve signaled measured rate cuts, borrowing costs remained elevated for small firms. The Bank of England’s base rate similarly stayed above historical averages, squeezing UK-based companies reliant on variable-rate credit lines. Meanwhile, the Reserve Bank of Australia navigated its own inflation fight, keeping rates at levels that increased mortgage repayments for business owners who had used personal property as collateral. All three economies share a common lesson: interest rate fluctuations and credit risk are not abstract concepts — they hit your bank account directly. Identifying financial risks in small business means tracking receivables aging, modeling worst-case revenue drops, and understanding your break-even point with surgical precision.

Read also: The Complete Guide to Personal Financial Management: Your Guide from Zero to Financial Stability

How Can Operational Risks Shut Down a Business Without Warning?

Operational risks live inside your processes. A key supplier in Shenzhen delays a shipment by 6 weeks. Your only refrigeration unit breaks down the night before a catering contract. Your head baker — the one who knows every recipe by heart — quits without notice. These events are not rare; they are statistically inevitable given enough time. Supply chain failures accelerated in visibility after the global disruptions of 2020–2022, and smaller firms felt the pain disproportionately because they lacked backup vendors. Equipment breakdowns cost US small businesses an estimated $50 billion annually in unplanned downtime, according to research published in the International Journal of Production Economics in 2021.

What Compliance and Legal Risks Should You Track Across Multiple Jurisdictions?

If you sell across borders — or even across state lines in the US — regulatory complexity multiplies fast. The US Department of Labor updated overtime threshold rules in 2024, catching thousands of small employers off guard. In Australia, the Fair Work Commission adjusts minimum wage annually, and the Australian Taxation Office (ATO) tightened reporting requirements for gig-economy contractors. The UK’s Making Tax Digital (MTD) program mandated digital VAT submissions, penalizing paper-based businesses that were slow to comply. Lawsuits, intellectual property disputes, and consumer protection claims round out this category. Compliance and legal risks are not dramatic — they are slow and expensive.

Read also: How to Comply with Banking Regulations in 2026: A Complete Guide

When Do Strategic Risks Become Existential Threats?

Strategic risks arise when the market shifts beneath your feet. A competitor launches a subscription model that undercuts your pricing by 30%. Consumer preferences pivot toward sustainability, and your packaging suddenly looks outdated. Brand reputation, once damaged by a viral social media post, can take years to rebuild. These threats require a different kind of vigilance — not internal audits, but external scanning. What are your competitors doing? What do your customers want next year, not just today?

How Real Is the Cyber and IT Risk for a Company With 10 Employees?

Very real. The 2023 Verizon Data Breach Investigations Report found that 43% of cyberattacks target small businesses. Ransomware does not discriminate by company size. A single phishing email opened by an intern can encrypt your entire customer database. Data breaches trigger regulatory fines under the General Data Protection Regulation (GDPR) in the UK and EU, the Australian Privacy Act, and various US state-level privacy laws like the California Consumer Privacy Act (CCPA). IT infrastructure failure — a crashed server, a corrupted backup — can halt operations for days. Cyber and IT risks are no longer a “big company problem.”

Read also: How to Secure Your Crypto Account: The Complete 2FA Setup Guide

How Do You Actually Create Your Small Business Risk Management Plan, Step by Step?

This is where theory becomes application. Follow these steps methodically, and by the end, you will hold a finished document — not a wish list.

Step 1: How Should You Identify Risks — the Brainstorming Phase?

Risk identification starts with a vulnerability audit. Gather your team — not just managers, but frontline staff who see operational cracks daily. Invite your external accountant or bookkeeper; they spot financial patterns you might miss. Use a simple prompt: “What could stop us from operating normally for one week or longer?” Write every answer down without judgment.

Walk through each department or function mentally. Sales: What if your top 3 clients left? Finance: What if your line of credit were frozen? IT: What if your cloud provider experienced a 48-hour outage? HR: What if a workplace injury triggered a lawsuit? This brainstorming session typically produces 15 to 40 distinct risks for a company with fewer than 50 employees. Do not edit the list prematurely. Completeness matters more than elegance at this stage.

A practical example brings this to life. Imagine Sarah, who owns a 12-person e-commerce business in Melbourne. She sells handmade skincare products online and through 3 retail partners. During her first risk identification session, her warehouse manager flagged that they stored all inventory in a single facility with no fire suppression system beyond basic extinguishers. Her accountant pointed out that 62% of revenue came from a single retail partner. Her IT contractor noted that website backups ran only once per month. None of these vulnerabilities were secrets — but nobody had written them down or assessed their severity until that afternoon. Within 2 hours, Sarah’s team documented 22 risks across all 5 categories. That list became the foundation of her small business risk management plan.

Read also: How to Set Up Bookkeeping for a New E-commerce Store Without Losing Your Mind

Step 2: How Do You Analyze and Assess Each Risk Using a Matrix?

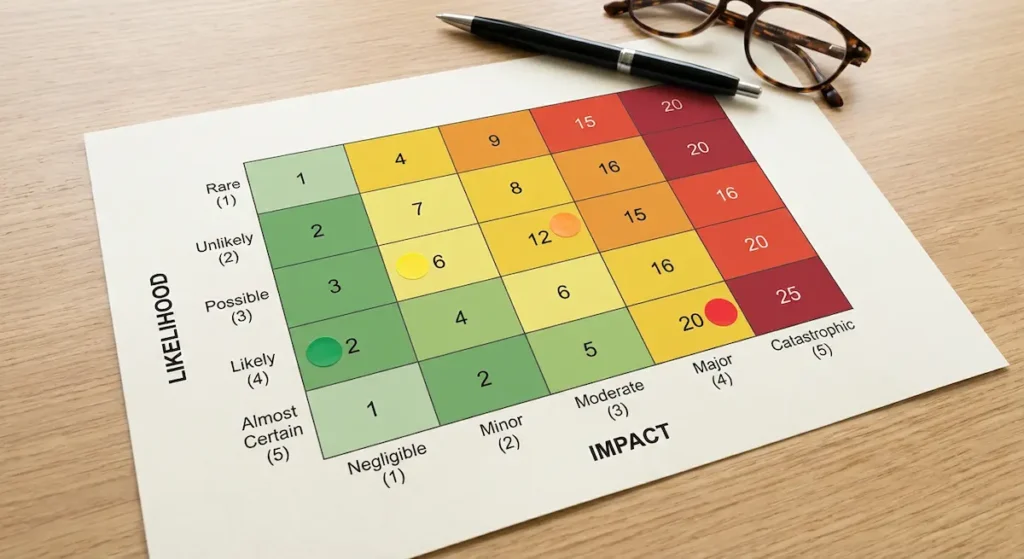

Once your risk list exists, the next task is scoring. This is where the Risk Assessment Matrix — sometimes called a Likelihood vs. Impact Matrix — enters the picture. The concept is straightforward. For each risk, assign two scores.

Likelihood measures how probable the event is. Use a scale of 1 (rare) to 5 (almost certain). Impact measures how severe the consequences would be if the event occurred, also on a 1-to-5 scale where 1 is negligible and 5 is catastrophic. Multiply the two numbers together. The resulting Risk Score (ranging from 1 to 25) tells you where each threat sits in your priority hierarchy.

Consider a practical application using Sarah’s e-commerce business. Her risk of losing the single large retail partner scored 4 on likelihood (the partner had been acquired by a larger company and was reviewing all vendor contracts) and 5 on impact (it represented 62% of revenue). That risk scored 20 out of 25 — an urgent, high-priority item demanding immediate attention. By contrast, the risk of a total website outage scored 2 on likelihood (her hosting provider had 99.9% uptime guarantees) and 3 on impact (she could redirect customers to a backup landing page within hours). That scored 6 — still worth monitoring, but not the top priority.

This business risk assessment template approach removes emotion from decision-making. You stop reacting to whichever risk feels scariest at 2 a.m. and start allocating resources where the math directs you.

Hamahplus Risk Assessment Matrix:

| Likelihood ↓ / Impact → | Negligible (1) | Minor (2) | Moderate (3) | Major (4) | Catastrophic (5) |

|---|---|---|---|---|---|

| Almost Certain (5) | 5 | 10 | 15 | 20 | 25 |

| Likely (4) | 4 | 8 | 12 | 16 | 20 |

| Possible (3) | 3 | 6 | 9 | 12 | 15 |

| Unlikely (2) | 2 | 4 | 6 | 8 | 10 |

| Rare (1) | 1 | 2 | 3 | 4 | 5 |

| Color Key: ■ Low Risk (1–7) ■ Medium Risk (8–11) ■ High Risk (12–16) ■ Critical Risk (17–25) Source: Framework adapted from COSO Enterprise Risk Management Framework, 2017 | |||||

Alt text: Hamahplus small business risk assessment matrix showing likelihood versus impact scoring grid for identifying financial risks in small business.

Step 3: Which Risks Deserve Immediate Funding — and Which Can Simply Be Watched?

Risk evaluation and prioritization separates the urgent from the merely significant. Divide your scored risks into 3 tiers. Tier 1 (scores 15–25) demands immediate action and budget allocation. Tier 2 (scores 8–14) requires documented contingency plans and quarterly monitoring. Tier 3 (scores 1–7) can be accepted and reviewed annually unless circumstances change.

Not every risk needs money thrown at it. Some need a procedural change — a new backup schedule, a revised contract clause, a second supplier relationship established. The goal of this step is not to eliminate all risk; that is impossible. The goal is to make a conscious, informed decision about which risks you will actively mitigate, which you will watch, and which you will accept as the cost of doing business. This evaluation stage is what transforms a raw brainstorming list into a functioning risk management process for small companies.

Step 4: What Are the 4 T’s of Risk Mitigation — and How Do You Choose the Right One?

With your prioritized list in hand, you now assign a mitigation strategy to each risk. The risk management profession relies on a framework called the 4 T’s — Tolerate, Treat, Transfer, and Terminate. Each represents a distinct posture toward a specific threat.

| Strategy | Action | Best Used When | Real-World Example | Cost to SMB |

|---|---|---|---|---|

| Tolerate (Accept) | Acknowledge the risk; take no active mitigation steps | Mitigation cost exceeds potential loss; risk score is Tier 3 (1–7) | A minor supplier raises prices by 5% — absorb the increase | $0 |

| Treat (Mitigate) | Reduce likelihood or impact through active controls | Risk is Tier 1 or 2; direct controls are feasible and affordable | Cross-train employees to eliminate single-point-of-failure roles | Low–Medium |

| Transfer | Shift financial impact to a third party | Impact is high but likelihood is moderate; insurance is cost-effective | Purchase cyber liability insurance ($500–$2,000/year for SMBs) | Medium |

| Terminate (Avoid) | Eliminate the activity that creates the risk | Risk is Tier 1 with no viable treatment; activity has low strategic value | Discontinue a low-margin product line with high liability exposure | Revenue Loss |

| Source: Framework based on HM Treasury — The Orange Book: Management of Risk — Principles and Concepts, UK Government, 2023 | ||||

Tolerate (Accept) means you acknowledge the risk exists but decide the cost of mitigation exceeds the potential loss. A Tier 3 risk — say, the unlikely chance that a minor supplier raises prices by 5% — often falls here. You accept it and move on. Treat (Mitigate/Reduce) means you take active steps to lower the likelihood or impact. Installing a firewall, diversifying your revenue streams, cross-training employees so no single departure cripples operations — these are treatments. Transfer means you shift the financial burden to another party. Insurance is the most common transfer mechanism. Business interruption insurance, professional indemnity insurance, and cyber liability insurance are all tools that move the financial impact away from your balance sheet. Outsourcing a high-risk function — such as data storage to a cloud provider with robust security certifications — also qualifies as transfer. Terminate means you stop doing the activity that creates the risk entirely. If a product line generates thin margins but exposes you to significant product liability claims, terminating it may be the smartest financial decision.

How, then, should a small business owner respond when a single risk seems to require multiple tactics? Apply them in layers. Sarah, from our Melbourne example, chose to treat her revenue concentration risk by actively pursuing 4 new retail partners while simultaneously tolerating the risk in the short term because severing the existing relationship prematurely would create a cash flow crisis. Layered strategies reflect the messy reality of running a real business.

Read also: Healthcare Risk Management Best Practices That Actually Work for Medical Facilities

Step 5: Why Must You Treat the Plan as a Living Document — and How Often Should You Review It?

A small business risk management plan that sits in a drawer gathers dust, not value. The document must evolve with your business. Set quarterly risk review meetings — 60 to 90 minutes, no longer. During each session, reassess your top Tier 1 risks. Have the scores changed? Has a new threat emerged? Did a mitigation strategy work, or does it need adjustment?

Assign a Risk Owner to each Tier 1 and Tier 2 item. This person is not necessarily responsible for fixing the risk; they are responsible for watching it and reporting changes. In a 10-person company, the owner might be you. In a 40-person company, it might be a department head. Accountability transforms a plan from a passive document into an active management tool.

Annual reviews should be more comprehensive. Revisit the entire risk register. Conduct a fresh brainstorming session. Factor in macroeconomic shifts — interest rate changes from the Federal Reserve, Bank of England, or Reserve Bank of Australia; new regulatory frameworks; shifts in consumer behavior post-pandemic. The risk landscape of 2025 looks different from 2023. Your plan should reflect that.

Read also: How to Set SMART Financial Goals (With Clear Examples)

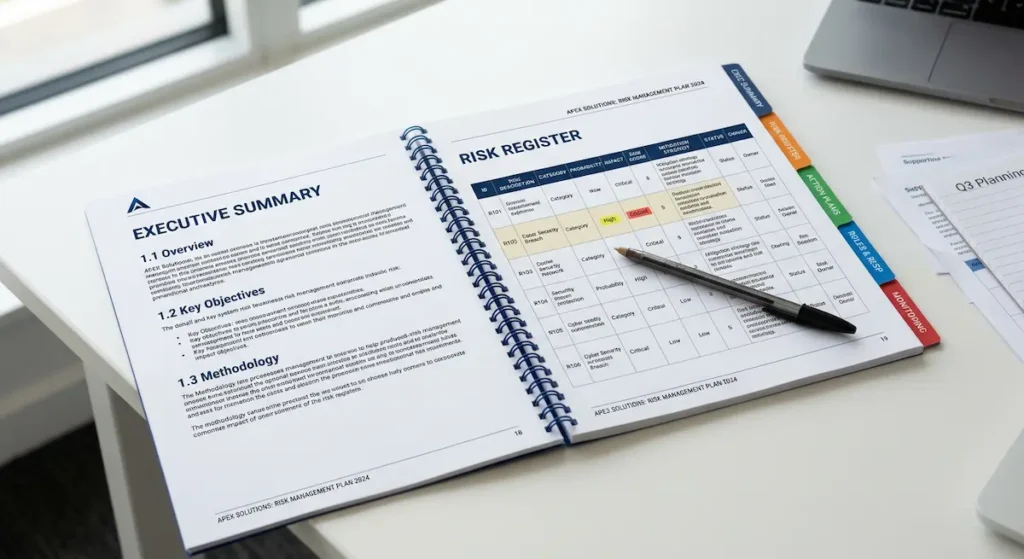

What Should Your Risk Management Document Actually Contain?

Structure matters. A risk management document that reads like stream-of-consciousness brainstorming will not impress a bank, an insurer, or a potential investor. Organize yours into clearly labeled sections:

- Executive Summary: A 1-page overview stating the company’s risk management philosophy, the date of last review, and the names of the individuals responsible for the plan.

- Risk Register: A spreadsheet or table listing every identified risk, its category (financial, operational, compliance, strategic, or cyber), its likelihood score, its impact score, its composite risk score, and its assigned mitigation strategy (Tolerate, Treat, Transfer, or Terminate).

- Action Plans: For each Tier 1 risk, a detailed description of the mitigation steps, the timeline, the budget allocated, and the person accountable.

- Roles and Responsibilities: A clear assignment of who monitors what. In small teams, one person may hold multiple roles — document this explicitly.

- Review Schedule: A calendar of quarterly and annual review dates, pre-set and non-negotiable.

- Appendices: Copies of relevant insurance policies, emergency contact lists, IT disaster recovery procedures, and regulatory compliance checklists.

| # | Document Section | What It Should Include | Typical Length | Update Frequency |

|---|---|---|---|---|

| 1 | Executive Summary | Company risk philosophy, date of last review, responsible personnel names | 1 page | Quarterly |

| 2 | Risk Register | Every identified risk with category, likelihood score, impact score, composite score, and assigned mitigation strategy | 2–4 pages (spreadsheet format) | Quarterly |

| 3 | Action Plans | Detailed mitigation steps for each Tier 1 risk, including timeline, budget, and accountable person | 1 page per Tier 1 risk | Quarterly |

| 4 | Roles & Responsibilities | Risk Owner assignments for each Tier 1 and Tier 2 item; clear accountability chain | 1 page | Annually |

| 5 | Review Schedule | Calendar of quarterly and annual review dates, pre-set and non-negotiable | 0.5 page | Annually |

| 6 | Appendices | Insurance policies, emergency contacts, IT disaster recovery procedures, compliance checklists | Variable (3–10 pages) | As needed |

| Source: Structure aligned with ISO 31000:2018 — Risk Management Guidelines, International Organization for Standardization | ||||

This structure creates a professional, actionable document that doubles as proof of due diligence. When an auditor, lender, or legal representative asks whether your company manages risk formally, you hand them this document.

Which Tools and Software Make Risk Management Affordable for Small Companies?

Enterprise-grade platforms like SAP GRC or MetricStream are priced for multinational corporations — well beyond the budget of most SMBs. Fortunately, a growing ecosystem of affordable, accessible tools exists. Here are categories worth exploring when evaluating the best risk management software for small business needs.

| Risk Category | Tool / Platform | Primary Function | Approximate Cost (Monthly) | Regions Supported |

|---|---|---|---|---|

| Financial Monitoring | QuickBooks | Cash flow tracking, receivables aging, expense alerts | $15–$100 | US, UK, AUS |

| Xero | Real-time financial dashboards, bank feed integration | $15–$78 | US, UK, AUS | |

| FreshBooks | Invoicing, expense tracking, late-payment alerts | $11–$55 | US, UK, AUS | |

| Compliance Tracking | Gusto | US payroll compliance, tax filing automation | $40 + $6/person | US |

| BrightHR | UK employment law updates, HR compliance tools | £5–£10/person | UK | |

| Employment Hero | Australian workplace regulation compliance | AUD $8–$14/person | AUS | |

| Cybersecurity | Bitdefender GravityZone | Endpoint protection, threat detection | $4–$8/device | Global |

| Duo Security (MFA) | Multi-factor authentication for all accounts | $3/user | Global | |

| Microsoft Defender for Business | Enterprise-grade security at SMB pricing | $3/user | Global | |

| Risk Register / Planning | Google Sheets / Excel | Custom risk register template, manual scoring | Free–$12.50 | Global |

| Notion | Custom risk databases, team collaboration | Free–$10/user | Global | |

| Source: Pricing verified as of Q1 2025. Security tool recommendations aligned with Australian Cyber Security Centre (ACSC) — Small Business Cyber Security Guide, 2023 | ||||

For financial monitoring, tools like QuickBooks, Xero, and FreshBooks provide real-time dashboards tracking cash flow, receivables aging, and expense anomalies. These platforms integrate with banking feeds across the US, UK, and Australia, giving you early warning when cash positions tighten. For compliance tracking, platforms like Gusto (US payroll compliance), BrightHR (UK employment law), and Employment Hero (Australian workplace regulations) automate regulatory updates so you are not blindsided by changes in labor law. For cybersecurity, solutions like Bitdefender GravityZone, CrowdStrike Falcon Go, and even Microsoft Defender for Business offer SMB-tier pricing with enterprise-level threat detection. Multi-factor authentication (MFA) tools such as Duo Security cost as little as $3 per user per month and eliminate a massive percentage of unauthorized access incidents.

For the risk register itself, a well-structured Google Sheets or Microsoft Excel template works for most small companies. Dedicated risk management platforms like LogicManager, Resolver, or even Notion (configured with custom databases) offer more sophisticated tracking if your business is growing rapidly. The critical point is this: do not let the lack of expensive software become an excuse to skip the planning process entirely. A spreadsheet and a quarterly meeting will outperform no plan at all, every single time.

Read also: Best Accounting Software for Mac Users: Top Picks with Built-In Inventory Management

How Do Regional Economic Conditions Affect Your Risk Priorities?

Global economic conditions shape the risk landscape differently depending on where your business operates. In the United States, the Federal Reserve’s monetary policy decisions ripple through small business borrowing costs with a delay of roughly 6 to 12 months. The 2023–2024 rate-hiking cycle pushed the federal funds rate to a 23-year high, and while easing began in late 2024, many small businesses still carried variable-rate debt priced at uncomfortable levels entering 2025. How to calculate risk impact for startups in this environment requires factoring in not just current rates, but projected rate trajectories published in the Federal Open Market Committee (FOMC) dot plot.

In the United Kingdom, Brexit-related trade frictions continue to create compliance and supply chain complexity for businesses importing from or exporting to the European Union. The UK Government’s Business Risk Portal notes that small exporters face additional customs declarations, rules of origin documentation, and potential tariff exposure that did not exist before 2021. These are not theoretical risks — they show up as real costs on profit-and-loss statements.

In Australia, geographic exposure to climate-related risks — bushfires, flooding, cyclones — adds a physical dimension to risk management that is less prominent in temperate US and UK regions. The Australian Prudential Regulation Authority (APRA) has pushed even small insurers to incorporate climate risk modeling, which affects the premiums small businesses pay for property and business interruption coverage. Understanding your regional risk profile is not optional; it is foundational to building a plan that actually works where you operate.

Read also: How SMEs Can Actually Access Trade Finance Without Getting Lost in Banking Bureaucracy

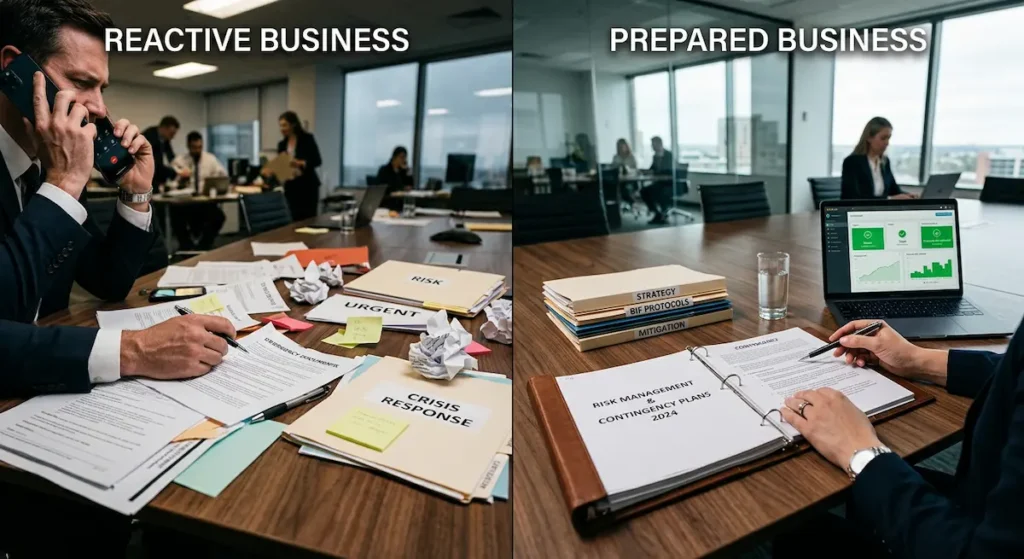

Can You Really Turn Risk into a Competitive Advantage?

Most business owners treat risk management as a defensive exercise — something you do to avoid losing. That framing is incomplete. A well-built small business risk management plan becomes a competitive weapon. Here is why. When your competitors scramble to react to a supply chain disruption, you already have a backup supplier activated. When a regulatory change catches your industry off guard, you have already adjusted because your quarterly review flagged the pending legislation 3 months ago. When a bank evaluates two loan applications — one from a company with a documented risk register and one without — the prepared company gets better terms.

Furthermore, the discipline of risk identification sharpens strategic thinking. The process forces you to ask hard questions about revenue concentration, customer dependency, operational fragility, and technological resilience. Those questions often surface opportunities: a second product line, a new market segment, a partnership that diversifies income. Risk management is not about fear. It is about clarity.

Mark Frigo, a professor of strategy and leadership at DePaul University’s Kellstadt Graduate School of Business, has written extensively on strategic risk management. His research argues that companies integrating risk analysis into strategic planning — not treating it as a separate compliance function — consistently outperform those that segregate the two disciplines. For a small company, this integration happens naturally because the same person often handles both strategy and risk.

Read also: Wealth Building: A Strategic Path to Financial Independence

What Mistakes Do Small Business Owners Make Most Often When Building Risk Plans?

Three errors recur with striking regularity. The first is treating the exercise as a one-time project rather than an ongoing discipline. A plan written in January 2024 and never revisited is dangerously outdated by July 2025. Markets shift. Regulations change. Staff turnover alters your operational capabilities.

The second mistake is ignoring low-probability, high-impact events — sometimes called “black swan” risks. These feel unlikely, so they get dismissed. The COVID-19 pandemic was a low-probability, catastrophic-impact event that decimated businesses without contingency plans. You cannot predict the specific black swan, but you can build financial buffers (cash reserves equal to 3–6 months of operating expenses, as recommended by the SBA) and operational flexibility (remote work capabilities, multiple supplier relationships) that improve resilience against any severe shock.

The third error is confusing insurance with risk management. Insurance is one tool — a transfer mechanism. It does not reduce the likelihood of a risk occurring; it only shifts the financial burden after the event. A comprehensive risk management process for small companies uses insurance alongside treatment, tolerance, and termination strategies. Relying solely on insurance leaves likelihood entirely unmanaged.

Read also: 5 Common Money Myths That Are Keeping You Poor (And What Actually Works)

What Does a Finished Small Business Risk Management Plan Look Like in Practice?

Let us return to Sarah in Melbourne and trace her completed document. Her executive summary states the company’s commitment to quarterly risk review, names Sarah as the Risk Management Lead, and identifies her accountant (David Chen, CPA) as the external advisor. Her risk register contains 22 entries organized by category, each scored on the likelihood-impact matrix, each assigned a mitigation strategy and a risk owner. Her top 3 Tier 1 risks — revenue concentration on a single retail partner, lack of fire suppression in the warehouse, and monthly-only website backups — each have detailed action plans.

For the revenue concentration risk, the action plan specifies: secure 2 new retail partners by Q3 2025, reduce the single-partner revenue share to below 40% by Q4 2025, and build a direct-to-consumer email marketing channel generating $5,000/month in independent revenue by year-end. Each action has a deadline, a responsible person, and a budget line. For the warehouse fire risk, the action plan prices a sprinkler system installation ($8,200 AUD, quoted by a licensed contractor), allocates the budget from Q2 cash reserves, and schedules installation for April. For the backup risk, the IT contractor moves the backup schedule from monthly to daily using an automated cloud service costing $29/month.

That document — roughly 12 pages including appendices — sits in a shared digital folder accessible to all team members. It is reviewed quarterly. It has already influenced a lending decision; Sarah’s bank noted the plan favorably during her credit line renewal in early 2025. This is what examples of risk management plans for small business look like in the real world — not theoretical, not corporate, but practical and immediate.

How Should You Start Building Your Plan Today?

Do not wait for the perfect moment. Open a blank document right now. Write the date and your company name at the top. List every risk you can think of in 15 minutes. Score each one on the likelihood-impact matrix. Identify your top 3. Assign a mitigation strategy to each. Congratulations — you have just created the first draft of your small business risk management plan. It is imperfect, and that is fine. Perfection is the enemy of preparedness. Refine it next quarter. Add more risks as you think of them. Bring your team into the conversation. The document will grow stronger every time you revisit it.

Risk is not the opposite of opportunity; it is the price of opportunity. Every business decision — hiring an employee, signing a lease, launching a product, entering a new market — carries uncertainty. The companies that thrive are not the ones that avoid risk. They are the ones that see it clearly, measure it honestly, and manage it deliberately. That is the discipline this plan gives you.

If you found this framework useful, visit Hamahplus to download a free, editable risk register template designed specifically for small businesses. Subscribe to the Hamahplus newsletter for monthly insights on financial planning, compliance updates across the US, UK, and Australia, and actionable strategies that keep your business resilient in uncertain times.

What is the single biggest risk your business faces right now — and what would you do differently if you scored it on the likelihood-impact matrix today?

Frequently Asked Questions

References and Bibliography

- Verbano, C., & Venturini, K. (2013). Managing Risks in SMEs: A Literature Review and Research Agenda. Journal of Technology Management & Innovation, 8(3), 186–197. DOI: 10.4067/S0718-27242013000400017

— A comprehensive literature review examining risk management practices specifically within small and medium-sized enterprises. - Brustbauer, J. (2016). Enterprise Risk Management in SMEs: Towards a Structural Model. International Small Business Journal, 34(1), 70–85. DOI: 10.1177/0266242614542853

— Research demonstrating how enterprise risk management frameworks can be adapted for resource-constrained small firms. - Verizon. (2023). 2023 Data Breach Investigations Report. https://www.verizon.com/business/resources/reports/dbir/

— Annual cybersecurity report documenting that 43% of data breaches involve small business victims. - Allianz Global Corporate & Specialty. (2023). Allianz Risk Barometer 2023. https://commercial.allianz.com/news-and-insights/reports/allianz-risk-barometer.html

— A global survey identifying business interruption and cyber incidents as the top business risks for multiple consecutive years. - U.S. Small Business Administration. (2024). Manage Your Business Risks. https://www.sba.gov/business-guide/manage-your-business

— Official US government resource providing foundational guidance on small business risk planning and continuity. - Australian Cyber Security Centre. (2023). Annual Cyber Threat Report 2022–2023. https://www.cyber.gov.au/about-us/reports-and-statistics/act-annual-cyber-threat-report-2022-2023

— Official Australian government report quantifying the average cost of cybercrime for small businesses at AUD $46,000. - UK Government. (2024). Business Risk Management Guidance. https://www.gov.uk/business-finance-and-support

— UK government portal covering business continuity, regulatory compliance, and risk resources for SMEs. - Federation of Small Businesses (FSB). (2020). Disruption and Resilience: The Impact of COVID-19 on Small Businesses. https://www.fsb.org.uk/resources-page/fsb-research.html

— UK survey finding that businesses with formal continuity plans were 2.5 times more likely to recover from COVID disruptions. - Sukumar, A., Edgar, D., & Grant, K. (2011). An Investigation of E-business Risks in UK SMEs. World Review of Entrepreneurship, Management and Sustainable Development, 7(4), 380–401. DOI: 10.1504/WREMSD.2011.042892

— Research paper examining digital and technology risks facing small enterprises in the United Kingdom. - Gao, S. S., Sung, M. C., & Zhang, J. (2013). Risk Management Capability Building in SMEs. Financial Management, 42(1), 37–62. DOI: 10.1111/fima.12002

— Study analyzing how small firms build internal risk management capabilities over time. - Frigo, M. L., & Anderson, R. J. (2011). Strategic Risk Management: A Foundation for Improving Enterprise Risk Management and Governance. Journal of Corporate Accounting & Finance, 22(3), 81–88. DOI: 10.1002/jcaf.20677

— Seminal paper arguing that risk management must be integrated into strategic planning for maximum effectiveness. - COSO. (2017). Enterprise Risk Management — Integrating with Strategy and Performance. Committee of Sponsoring Organizations of the Treadway Commission. https://www.coso.org/guidance-on-ic/erm-framework

— The definitive ERM framework used globally, adaptable for businesses of all sizes. - Hopkin, P. (2018). Fundamentals of Risk Management: Understanding, Evaluating and Implementing Effective Risk Management (5th ed.). Kogan Page.

— A comprehensive textbook covering risk management principles from identification through monitoring. - Lam, J. (2014). Enterprise Risk Management: From Incentives to Controls (2nd ed.). Wiley.

— Foundational book bridging theoretical ERM frameworks with practical business implementation. - The Economist. (2024). “Small Businesses and the Cost of Risk.” The Economist, Finance & Economics Section. https://www.economist.com/

— Accessible analysis of how macroeconomic uncertainty disproportionately impacts small business planning.

Further Reading and Resources for Deeper Exploration

1. Hillson, D. (2016). The Risk Management Handbook: A Practical Guide to Managing the Multiple Dimensions of Risk. Kogan Page.

Why we recommend this: This handbook provides an exhaustive, practitioner-oriented treatment of every risk management dimension — from financial to reputational to project-based risk — with worksheets and templates suitable for both beginners and experienced professionals.

2. Kaplan, R. S., & Mikes, A. (2012). “Managing Risks: A New Framework.” Harvard Business Review, 90(6), 48–60.

Why we recommend this: This landmark HBR article introduced a widely cited classification of risk types (preventable, strategic, and external) and proposed governance structures that small business owners can scale down to their own operations.

3. ISO 31000:2018. Risk Management — Guidelines. International Organization for Standardization.

Why we recommend this: ISO 31000 is the global standard for risk management principles and processes. Reading the standard itself (available for purchase through ISO or national standards bodies) gives students and researchers the foundational vocabulary and conceptual architecture upon which all modern risk management practice is built.

This article has been reviewed by the editorial board at Hamahplus to ensure accuracy and factual integrity. Sources cited in this piece were cross-referenced with publicly available data from government agencies, peer-reviewed journals, and recognized industry bodies. This content is intended for educational purposes and does not constitute personalized financial, legal, or insurance advice. Readers should consult qualified professionals for decisions specific to their business circumstances.

Federal Reserve: Maintains supervisory guidance on risk management for banking organizations and borrowing standards affecting small business lending. Federal Reserve Supervisory & Regulatory Framework

SEC: Regulates financial disclosures and risk reporting requirements for publicly listed companies that impact SMB supply chains and partnerships. SEC Regulatory Framework

CFPB: Enforces consumer financial protection standards relevant to small businesses offering consumer-facing financial products. CFPB Consumer Protection Standards

FCA: The Financial Conduct Authority oversees operational resilience requirements that apply to financial services SMBs and firms regulated under FCA PS21/3. FCA Operational Resilience Guidelines

HM Treasury: Publishes The Orange Book, the UK government’s foundational framework for risk management principles across all sectors. HM Treasury — The Orange Book

ASIC: The Australian Securities and Investments Commission regulates corporate governance and risk disclosure for Australian businesses. ASIC Corporate Governance Resources

APRA: The Australian Prudential Regulation Authority sets prudential standards (CPS 220 — Risk Management) affecting insurers and financial institutions that serve small businesses. APRA Risk Management Standards